No votes yet.

Average American Spending by Category: Key Statistics and Trends

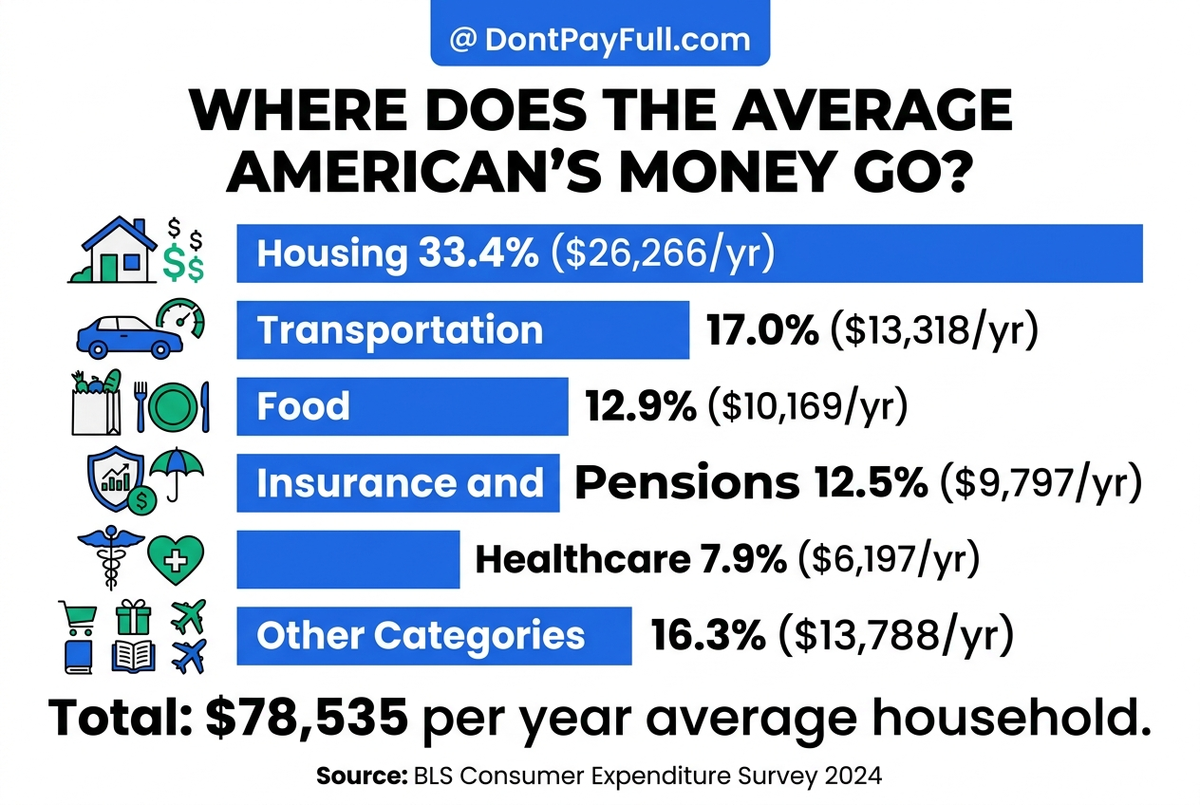

The average American household spent $78,535 in 2024 across 14 budget categories. This breakdown uses 2024 BLS data to show where money actually goes, how income level shifts the picture, and which spending categories have real savings potential.

The Bureau of Labor Statistics released its Consumer Expenditure Survey for 2024 in February of this year, and the headline number landed with a thud for a lot of households: $78,535. That’s what the average American consumer unit spent last year, on everything from rent to gas to that streaming subscription you keep meaning to cancel. Spread across 12 months, it’s $6,545 going out the door every single month.

But that number hides a lot. Not every category is created equal, and not every household has the same ability to cut back. This guide breaks down where that $78,535 actually goes, how spending shifts by income and age, and where deals and coupons can actually move the needle.

Our team reviews deal activity across thousands of retailers, and one thing stands out when looking at this BLS data: most of the budget is locked up in categories where coupons can’t help at all. Knowing which slice is actually flexible is the first step to saving real money.

Key Takeaways

- ✓ The average American household spent $78,535 in 2024, or about $6,545 per month, per the most recent BLS Consumer Expenditure Survey.

- ✓ Housing is the single largest expense at $26,266 (33.4% of the budget), followed by transportation at $13,318 (17%).

- ✓ Healthcare was the fastest-growing major category in 2024 at +5.3% year-over-year, while entertainment was the only category to shrink.

- ✓ The lowest-income households spend 43% of their budget on housing vs. just 29% for the highest earners, a 14-point gap that grows wider every year.

- ✓ Only about 27% of total spending falls in truly flexible categories where deals, coupons, and behavior changes can realistically reduce costs.

Overview: How Much Does the Average American Spend?

The average American consumer unit spent $78,535 in 2024, up from $77,280 in 2023. That works out to roughly $6,545 per month. Pre-tax income for the same average household was $92,404, meaning households are spending about 85 cents of every dollar they earn.

Overview Statistics

- Average annual household spending reached $78,535 in 2024, a $1,255 increase from 2023.

- Average income before taxes was $92,404, putting the spending-to-income ratio at roughly 85%.

- The typical consumer unit consists of 2.5 persons with 1.4 earners, an average age of 51.3 years.

- 66% of consumer units own their home, which shapes how housing costs show up in the data.

- The personal saving rate stood at 4.1% in January 2026, near multi-decade lows.

- US total consumer spending reached an annualized rate of $19.2 trillion in Q4 2025, per the Bureau of Economic Analysis.

- Americans aged 35-44 spend the most of any age group, averaging over $90,000 per year.

A quick note on what “consumer unit” means. The BLS doesn’t just count nuclear families. A consumer unit can be a single person, a couple, a multigenerational household, or any group sharing major expenses. Because the 130,000 households surveyed represent the full spectrum of American living arrangements, this average reflects real diversity, not just an idealized family of four.

The spending-to-income gap tells an important story. After spending, roughly $13,869 is left before taxes take their cut. And with the personal saving rate near historic lows, many households are running far thinner than that 15% cushion suggests. That’s before factoring in the $1.21 trillion in credit card debt US households were carrying as of Q4 2024, per the Federal Reserve Bank of New York. The $78,535 average includes people spending well above their income by borrowing. Plain and simple.

Average American Spending by Category (2024)

The top five spending categories make up roughly 83% of the average household budget, leaving the remaining 14 categories to split about $13,400. Housing alone takes more than the bottom nine categories combined.

Spending by Category Statistics

- Housing is the largest budget category at $26,266 per year, representing 33.4% of all spending.

- Transportation ranks second at $13,318 (17%), followed by food at $10,169 (12.9%).

- Personal insurance and pensions reached $9,797 (12.5%), rising 5.1% year-over-year.

- Healthcare spending hit $6,197 (7.9%), the fastest-growing major category at +5.3% YoY.

- Entertainment fell to $3,609, contracting 0.7% year-over-year, the only major category to shrink in 2024.

- Apparel and services totaled $1,985, while education reached $1,546.

- The smallest tracked category, reading, came in at just $158 per year.

Here’s the full breakdown from the 2024 BLS Consumer Expenditure Survey:

| Category | Annual Amount | Monthly Amount | % of Total | YoY Change |

|---|---|---|---|---|

| Housing | $26,266 | $2,189 | 33.4% | +3.3% |

| Transportation | $13,318 | $1,110 | 17.0% | +1.1% |

| Food | $10,169 | $847 | 12.9% | +1.8% |

| Personal Insurance & Pensions | $9,797 | $816 | 12.5% | +5.1% |

| Healthcare | $6,197 | $516 | 7.9% | +5.3% |

| Entertainment | $3,609 | $301 | 4.6% | -0.7% |

| Cash Contributions | $2,560 | $213 | 3.3% | – |

| Apparel & Services | $1,985 | $165 | 2.5% | – |

| Education | $1,546 | $129 | 2.0% | – |

| Miscellaneous | $1,156 | $96 | 1.5% | – |

| Personal Care | $774 | $65 | 1.0% | – |

| Alcoholic Beverages | $600 | $50 | 0.8% | – |

| Tobacco Products | $300 | $25 | 0.4% | – |

| Reading | $158 | $13 | 0.2% | – |

| Total | $78,535 | $6,545 | 100% |

The YoY columns with “-” reflect categories where the BLS didn’t publish a comparison figure in the 2024 release. The four categories where annual change data is available tell a clear story: healthcare and insurance are pulling money away from entertainment, which shrank even as most other categories grew.

Annual Spending by Major Category (2024)

Average US household, BLS Consumer Expenditure Survey 2024

Housing$26,266

Transportation$13,318

Food$10,169

Insurance & Pensions$9,797

Healthcare$6,197

Entertainment$3,609

Total annual spending: $78,535

Housing: The Largest Budget Category

Housing costs the average household $26,266 per year, roughly one-third of everything they spend. That’s $2,189 per month, and it rose 3.3% from 2023. Shelter alone, meaning rent or the equivalent for homeowners, accounts for $15,699 of that figure.

Housing Statistics

- Total housing spending averages $26,266 per year, up 3.3% from 2023’s $25,436.

- Shelter (rent or owner equivalent) is the largest subcategory at $15,699, representing 20% of all household spending.

- Utilities, fuels, and public services add another $4,715 per year, or about $393 per month.

- Household furnishings and equipment cost an average of $2,098 per year.

- Household operations (services like cleaning and lawn care) total $1,545 annually.

- Housekeeping supplies round out housing at $836 per year.

- 66% of consumer units own their homes, meaning renter cost profiles look significantly different from this average.

Shelter alone at $15,699 is more than food and healthcare combined. That’s a useful way to feel the weight of housing in the American budget: you could eat every meal out and still not match what you pay for the roof overhead.

The subcategory breakdown shows where there’s some wiggle room. Rent, mortgage payments, and utilities are largely fixed. But furnishings ($2,098) and housekeeping supplies ($836) together total nearly $3,000 per year. Both are categories where coupons apply directly. Retailers like IKEA, Wayfair, and Home Depot run frequent promotions on home goods. Home improvement stores like Lowe’s run seasonal discounts that can take a real bite out of those numbers.

The 3.3% year-over-year housing increase hits renters hardest. Homeowners with fixed-rate mortgages are somewhat insulated. But the 34% of consumer units who rent are absorbing market-rate increases that run well above that average, especially in coastal metros. For them, housing’s share of the budget easily exceeds the 33.4% national figure.

Transportation Spending: Car Dependency Costs American Households $13,318

Transportation is the second-largest spending category at $13,318 per year, or $1,110 per month, and it grew 1.1% from 2023. The US transportation budget is almost entirely built around car ownership: vehicle purchases, maintenance, and fuel together total $12,389, leaving just $929 for public transit.

Transportation Statistics

- Total transportation spending is $13,318 per year, representing 17% of the average household budget.

- Vehicle purchases alone average $4,987 per year, accounting for new and used car acquisitions prorated across the survey sample.

- Other vehicle expenses (insurance, maintenance, repairs) cost an additional $4,559 annually.

- Gasoline and motor oil spending totaled $2,843 per year, down from 2022 highs.

- Public transportation, including airfare, buses, and trains, accounts for just $929 per year on average.

- Car-related costs (purchase + maintenance + fuel) equal $12,389, or 93% of total transportation spending.

The $4,559 “other vehicle expenses” figure is the most underappreciated line in the transportation budget. That’s insurance premiums, oil changes, tire replacements, and the repair nobody budgeted for. Big category. It’s also one area where savvy shoppers can find relief. Auto parts retailers like AutoZone and O’Reilly run regular discount events, and comparison shopping on insurance premiums can shift hundreds of dollars per year.

What most household budget guides miss is how dramatically car dependency inflates US transportation costs. The $929 in public transit spending is a tiny share of the total. For households in car-dependent suburban or rural areas, that transit number is essentially zero. So the $13,318 average understates the situation for many households who spend more on vehicle financing and fuel alone.

Food Spending: At Home vs. Dining Out

Americans spent an average of $10,169 on food in 2024, up 1.8% from 2023, and the split between cooking at home and dining out shows just how much our eating habits have changed. Of that total, $5,853 goes to food at home (groceries) and $4,316 to food away from home (restaurants, takeout, delivery).

Food Spending Statistics

- Total food spending averages $10,169 per year, or $847 per month.

- Food at home (groceries) accounts for $5,853, or 58% of total food spending, at roughly $488 per month.

- Food away from home (restaurants, takeout, delivery) totals $4,316, or 42% of food spending, at roughly $360 per month.

- Food away from home has grown faster than grocery spending over the past decade, reflecting a structural shift toward convenience.

- The 1.8% year-over-year increase in food spending follows several years of elevated grocery inflation.

- Food is the most coupon-accessible major spending category, with grocery deals and restaurant promotions widely available year-round.

The 58/42 split between home cooking and dining out is tighter than most people assume. A decade ago, the split was closer to 65/35. That shift reflects higher convenience expectations and the growth of delivery apps that turned restaurant food into a daily habit. Fewer households have time to cook every night. And the apps make skipping it easy.

Food Spending: At Home vs. Away

Food at Home58% ($5,853/yr)

Food Away42% ($4,316/yr)

So what can actually move the food number? Food is the category where coupons and deals have the highest real-world impact on a household budget. Grocery coupons, store loyalty cards, cashback apps, and restaurant promotions all target this $847 monthly line directly. Tracking deals across hundreds of food and grocery retailers, a pattern keeps showing up: households that actively use grocery promotions can realistically shave 10-15% off their at-home food costs, which translates to roughly $50-$75 per month in savings, or $600-$900 per year.

💡

Tip: The $360 per month spent on dining out is also the most flexible part of the food budget. Even swapping two restaurant meals per week for home cooking can cut $100-$150 monthly from this line.

Healthcare Spending Trends

Healthcare costs hit $6,197 per household in 2024, a 5.3% jump from $5,885 in 2023, and it’s the fastest-growing major spending category for American families. That $312 annual increase might sound modest, but compounded at this rate, healthcare is poised to consume an even larger share of the budget over the next decade.

Healthcare Statistics

- Average household healthcare spending hit $6,197 in 2024, up 5.3% year-over-year from $5,885 in 2023.

- Healthcare represents 7.9% of the average household budget, but this share rises sharply with age.

- The bottom income quintile spends 9.5% of their budget on healthcare vs. 6.4% for the highest earners.

- Healthcare spending is projected to grow at 5-6% annually through 2030, per a Deloitte Health Care Cost Survey.

- Adults aged 65-74 allocate the highest share of income to healthcare of any age group.

- The 5.3% YoY growth in healthcare outpaces housing (3.3%), food (1.8%), and transportation (1.1%).

The 5.3% growth rate isn’t a one-year blip. Healthcare has risen steadily for years, driven by premium increases, higher deductibles, and prescription drug costs. The Deloitte Health Care Cost Survey projects 5-6% annual growth through 2030. At that pace, today’s $6,197 could reach $8,000-$9,000 by the end of the decade. That’s a big shift in the household budget.

The income disparity is stark. Lower-income households often lack employer-sponsored coverage. So they spend a higher percentage on healthcare with less budget room to absorb it. The top quintile’s 6.4% share is still more dollars in absolute terms. But a $6,197 healthcare bill hits very differently on a $28,000 budget than it does on a $138,000 one.

Where can households find relief? Prescription savings programs, generic drug substitutions, and FSA accounts for tax-advantaged spending are all valid ways to save. For over-the-counter products, pharmacy coupons at Walgreens and CVS can offset a slice of recurring costs. The big-ticket items, premiums and deductibles, are largely non-negotiable. But the small stuff adds up.

Entertainment, Apparel, and Other Discretionary Spending

Discretionary spending, the non-essentials, totals roughly $8,814 combined for the average household. These five categories are also where you’ll get the most mileage out of coupons, sales events, and careful budgeting.

Discretionary Spending Statistics

- Entertainment spending averaged $3,609 in 2024, down 0.7% year-over-year, the only major category to contract.

- Apparel and services totaled $1,985 per year (2.5% of total spending), or about $165 per month.

- Education spending reached $1,546 per year (2.0%), though this varies widely by household.

- Personal care products and services cost an average of $774 annually.

- Alcoholic beverages averaged $600 per year, with tobacco products at $300.

- These five categories combined represent roughly 11.2% of total household spending.

Entertainment’s 0.7% decline in 2024 is notable. It’s a small contraction, but it tells a story. Households pulled back on fun as housing and healthcare costs rose. That makes sense. When fixed costs grow faster than income, flexible categories take the hit first.

Apparel is particularly interesting from a deals perspective. The $1,985 annual figure covers everything from fast fashion basics to occasional big purchases. But this is a category where deal timing matters enormously. Retailers like Target and major clothing chains run end-of-season clearances where prices drop 50-70% off original retail. From processing millions of coupon codes across apparel categories, it’s clear that this is one of the highest-coupon-activity spending categories on DontPayFull, with redemption rates spiking heavily in January (winter clearance) and July (summer clearance).

Personal care at $774 per year is smaller in absolute terms, but it’s entirely made up of frequently purchased items where coupons are always available. Shampoo, skincare, toiletries, and salon services are among the most actively promoted product categories in retail.

How Spending Varies by Income Level

The income quintile breakdown is where the spending data gets sobering. The average $78,535 figure masks a range from $28,234 at the bottom quintile to $138,650 at the top, with dramatically different budget compositions at each level.

Income Level Statistics

- Bottom 20% of households (income roughly under $35,046) spend just $28,234 per year total.

- Top 20% of households (income over $150,342) spend $138,650 per year, nearly 5x more than the lowest quintile.

- Housing consumes 43% of the bottom quintile’s budget, compared to 29% for the top quintile, a 14-point gap.

- Food takes 17% of the lowest earners’ spending vs. 10.5% for the highest, showing similar proportional compression.

- The Federal Reserve’s distributional accounts put the Gini coefficient for consumption spending at 0.31-0.33.

- The top 20% account for approximately 40% of total US personal consumption; the bottom 20% account for roughly 9%.

The housing burden gap is the sharpest sign of income inequality in the spending data. A household spending 43% on housing has almost nothing left for financial resilience. Once food, transportation, and healthcare are covered, discretionary spending essentially disappears. For the bottom quintile, that’s most of the budget gone to basics.

| Income Quintile | Total Spending | Housing % | Food % | Healthcare % |

|---|---|---|---|---|

| Lowest 20% (under ~$35,046) | $28,234 | 43.0% | 17.0% | 9.5% |

| Second 20% ($35,046-$55,000) | $44,521 | 37.2% | 14.1% | 9.2% |

| Middle 20% ($55,000-$82,000) | $61,870 | 34.1% | 13.0% | 8.0% |

| Fourth 20% ($82,000-$130,000) | $87,304 | 31.5% | 11.8% | 7.1% |

| Highest 20% (over $150,342) | $138,650 | 29.0% | 10.5% | 6.4% |

This pattern holds for all essential categories. As income rises, necessities take a smaller share of the budget. More room opens up for discretionary spending, saving, and investing. Economists call this Engel’s Law, and it holds true in the modern American data.

Here’s what this means for anyone trying to stretch their dollars. Lower-income households benefit most, in percentage terms, from any savings on essentials. A $50 grocery coupon is a bigger deal on a $28,000 budget than on a $138,000 one. This is why deal-seeking skews heavily toward the bottom two quintiles. Every dollar of savings has more impact there.

American Spending by Age Group: From Peak Earners to Retirees

Spending isn’t static across a lifetime. Americans in peak earning and family formation years spend the most in total, while the composition of spending shifts dramatically as households move through different life stages.

Age-Based Spending Statistics

- Americans aged 35-44 have the highest total spending, averaging over $90,000 per year, covering peak family formation costs.

- Adults 25-34 carry the highest housing cost share, as this cohort faces both peak rental rates and first-home purchase costs.

- Transportation spending peaks in the 45-54 age range, when multi-vehicle households reach their maximum size.

- Healthcare’s share of spending rises consistently with age, becoming dominant for adults 65 and older.

- Millennials (roughly ages 28-43) now represent the largest share of consumer spending, surpassing Baby Boomers, per Morgan Stanley research.

- Remote work contributed to a 4-5% increase in home-related spending (furniture, utilities, broadband) between 2020 and 2023, per McKinsey.

The spending lifecycle follows a predictable curve. Young adults in their late 20s and early 30s are absorbing high housing costs, often while paying down student loans. Their total spending is constrained by lower incomes. Peak spending hits in the 35-44 range, when family size, career earnings, and major purchases all converge. By the late 40s and 50s, transportation peaks as households add vehicles.

Retirement changes the picture. For homeowners who’ve paid off their mortgages, housing costs drop. But healthcare costs rise sharply. Adults aged 65-74 spend a higher share of income on healthcare than any other age group. That shift from housing burden to healthcare burden shows up consistently in the BLS data year after year.

The Millennial cohort’s rise as the largest consumer spending group is significant. Millennials came of age during the 2008 financial crisis and entered a rough labor market. Now they face housing costs that are much higher relative to income than prior generations experienced. That context explains why this cohort leans heavily into value-seeking: coupons, cashback apps, deal-hunting before major purchases. It’s not a personality trait. It’s a rational response to a tighter budget.

Spending Trends: How American Budgets Have Changed

The clearest trend in American household spending over the past two years is a divergence between survival spending and enjoyment spending. Healthcare and insurance are taking larger bites, while entertainment contracted.

Spending Trend Statistics

- Healthcare grew 5.3% in 2024 and has grown at roughly 5%+ annually for several consecutive years.

- Personal insurance and pensions rose 5.1% in 2024, driven partly by higher retirement contribution rates.

- Housing costs increased 3.3% year-over-year in 2024, following similar increases in 2022 and 2023.

- Food spending grew 1.8% in 2024, a deceleration from the elevated food inflation of 2021-2023.

- Entertainment declined 0.7% in 2024, the only major category to contract.

- US household credit card debt reached $1.21 trillion in Q4 2024, a record level per the Federal Reserve Bank of New York.

The contrast between healthcare (+5.3%) and entertainment (-0.7%) is striking. Households are cutting discretionary spending to fund the non-negotiable cost increases. Economists call this “crowding out.” Fixed cost growth eats the budget space that used to go to fun.

Record credit card debt at $1.21 trillion is the other side of this story. When spending grows faster than income, debt fills the gap. The $78,535 average includes households actively borrowing to stay afloat. The data doesn’t show that directly. But the $1.21 trillion does.

🤔

Did You Know: Food inflation, which ran 6-8% per year in 2022 and 2023, has moderated to under 2% in 2024, making grocery budgets one of the few places where the pressure has eased recently.

The three-year housing trend is also telling. Housing has risen 3-4% per year since 2022. That sounds moderate, but it compounds. A household paying $24,000 in housing costs was paying over $26,000 two years later. Nothing improved. It just cost more. For renters, the increases can run even steeper.

Where Americans Can Save: Fixed vs. Flexible Spending

Not all spending is equal. Some categories are locked in; others can flex. The simplest way to think about your budget is to sort the 14 BLS categories into fixed, semi-fixed, and flexible buckets.

Savings Opportunity Statistics

- Fixed spending (housing, insurance, utilities) accounts for roughly $44,000 per year, or about 56% of the average budget.

- Flexible spending (dining out, entertainment, apparel, personal care) totals roughly $21,000 per year, or about 27% of the budget.

- Semi-fixed spending (groceries, transportation fuel, healthcare OTC) sits in between at roughly $13,500, or about 17%.

- A 10-15% reduction in flexible spending alone would save the average household $2,100-$3,150 per year.

- Food away from home ($4,316) and entertainment ($3,609) together represent $7,925 per year in highly couponing-accessible spending.

- Apparel ($1,985) and personal care ($774) add another $2,759 in deal-accessible annual spending.

Here’s the framework in table form:

| Category | Annual Amount | Flexibility | Deal/Coupon Potential |

|---|---|---|---|

| Housing – Shelter | $15,699 | Fixed | Very Low |

| Housing – Utilities | $4,715 | Semi-fixed | Low (some energy savings) |

| Vehicle Purchases | $4,987 | Semi-fixed | Low (timing matters) |

| Vehicle Maintenance | $4,559 | Semi-fixed | Medium (auto parts deals) |

| Insurance & Pensions | $9,797 | Fixed | Very Low |

| Healthcare – Premiums | ~$4,000 | Fixed | Very Low |

| Gasoline | $2,843 | Semi-fixed | Low (cashback cards) |

| Food at Home | $5,853 | Flexible | High (grocery coupons) |

| Food Away from Home | $4,316 | Flexible | High (restaurant deals) |

| Entertainment | $3,609 | Flexible | High (event, streaming deals) |

| Apparel & Services | $1,985 | Flexible | Very High (seasonal sales) |

| Personal Care | $774 | Flexible | High (pharmacy coupons) |

| Education | $1,546 | Semi-fixed | Medium (student discounts) |

| Housekeeping & Furnishings | $2,934 | Flexible | High (home goods deals) |

The “Very High” deal potential categories are precisely where DontPayFull’s Chrome extension surfaces working codes automatically. Apparel, personal care, home goods. Those are the categories where consumers leave the most money on the table by not checking for discounts before checkout.

What most budget guides miss is that the real savings opportunity isn’t in the biggest categories. It’s in the most coupon-saturated ones. You can’t coupon your way to a lower rent check. But apparel deals regularly hit 30-50% off at end of season. Grocery promotions compound across every weekly shop. Over a year, consistent coupon use in flexible categories can realistically save $2,000-$3,000.

Methodology

This article draws primarily from the BLS Consumer Expenditure Survey 2024, released by the Bureau of Labor Statistics in February 2026.

A note on data currency: Government statistical agencies typically publish annual survey results 12-18 months after the reference year closes. The BLS Consumer Expenditure Survey for 2024 was released in February 2026, making it the most current data available at the time of writing. Where this article references 2023 or earlier comparison figures, those reflect prior-year BLS releases, not outdated research.

The BLS CES uses about 130,000 interview surveys conducted annually by the Census Bureau on behalf of BLS. The survey unit is a “consumer unit,” defined broadly as either a single consumer or a group of related or unrelated individuals who share living expenses. Consumer units include single-person households, families, and any group with shared finances, not strictly nuclear families. This means the “average” household in this data reflects real diversity in household composition, income, and spending habits.

Supplementary data in this article comes from several additional sources:

– Federal Reserve distributional national accounts for consumption inequality data (Gini coefficients, quintile shares of total PCE)

– Bureau of Economic Analysis for total US personal consumption expenditure figures

– Federal Reserve Bank of New York consumer credit data for household debt figures

– Deloitte Health Care Cost Survey (2024) for healthcare spending projections

– Morgan Stanley consumer research for generational spending share data

– McKinsey & Company analysis for remote work spending impact estimates

These figures are averages across the survey sample. Individual household spending varies significantly based on income, family size, geographic location, homeownership status, and lifestyle choices. The BLS CES is the most comprehensive and authoritative source available for US household spending patterns.

Data compiled by the DontPayFull Research Team based on publicly available data from government agencies, academic institutions, and industry research firms.

The Bottom Line

The average American household spends $78,535 per year, but that number is largely locked up in fixed costs. Housing alone takes $26,266 (one-third of the total), and healthcare is rising at 5.3% per year with no signs of slowing. Only about 27% of the average budget sits in flexible categories where deals, coupons, and intentional choices can actually reduce spending. Focus your saving efforts on food (especially dining out at $4,316/year), entertainment ($3,609), apparel ($1,985), and personal care ($774). Those four categories combined offer $10,700 per year in genuine deal-accessible spending, where consistent coupon use can realistically save $1,500-$2,000 annually.

FAQ

What is the average American’s monthly spending?

The average American consumer unit spends about $6,545 per month, based on the BLS Consumer Expenditure Survey 2024. Annual spending totals $78,535. The monthly figure breaks down as roughly $2,189 for housing, $1,110 for transportation, $847 for food, $816 for insurance and pensions, and $516 for healthcare.

What do Americans spend the most money on?

Housing is by far the largest expense category, accounting for $26,266 per year or 33.4% of the average budget. Transportation comes in second at $13,318 (17%), followed by food at $10,169 (12.9%). These three categories alone represent about 63% of total household spending.

How much does the average American spend on housing?

The average American household spends $26,266 per year on housing, broken down as $15,699 for shelter (rent or owner-equivalent), $4,715 for utilities and fuels, $2,098 for furnishings, $1,545 for household operations, and $836 for housekeeping supplies. Housing costs rose 3.3% from 2023 to 2024.

What percentage of income should go to each budget category?

Common guidelines suggest 30% for housing, 15% for transportation, 10-15% for food, and 10% for healthcare and insurance. The actual BLS averages run close to these for housing (33.4%) and food (12.9%), but healthcare (7.9%) is below the recommended threshold while insurance and pensions (12.5%) run higher than many budgeting rules anticipate.

How does American spending compare by income level?

The top 20% of households spend nearly five times as much as the bottom 20%, $138,650 vs. $28,234 per year. But the composition differs significantly: lower-income households spend 43% of their budget on housing vs. 29% for top earners. Lower-income households also spend a larger share on food and healthcare. The Federal Reserve estimates the top 20% account for roughly 40% of all US consumer spending.

How much does the average American spend on food per month?

The average household spends $847 per month on food, split between $488 on groceries (food at home) and $360 on restaurants and takeout (food away from home). Food spending totals $10,169 per year and rose 1.8% from 2023 to 2024.

What percentage of Americans live paycheck to paycheck?

The BLS data shows significant financial fragility in American households. With the personal saving rate near 4% of disposable income and household credit card debt at a record $1.21 trillion as of Q4 2024, a substantial share of Americans have little financial buffer. The median real household income of $80,610 (Census Bureau, 2023) sits just above average spending levels, leaving limited room for savings at typical income levels.

Sources

- Bureau of Labor Statistics, Consumer Expenditures 2024: Official BLS release with complete 2024 CES data, including major categories, subcategories, YoY comparisons, and income quintile breakdowns (February 2026)

- Federal Reserve, Distributional National Accounts: Methods and estimates for US consumption inequality, Gini coefficients, and quintile shares of total PCE (2023)

- Federal Reserve Bank of New York, Consumer Credit: Household credit card debt reaching $1.21 trillion in Q4 2024

- Bureau of Economic Analysis: US total personal consumption expenditure data, annualized rate Q4 2025

- Deloitte Health Care Cost Survey 2024: Healthcare spending growth projections of 5-6% annually through 2030

- Morgan Stanley Research 2024: Millennial consumer spending surpassing Baby Boomers as largest cohort

- McKinsey & Company 2023: Remote work contribution to 4-5% increase in home-related spending 2020-2023

Do You Have Any Suggestions?

We're always looking for ways to enrich our content on DontPayFull.com. If you have a valuable resource or other suggestion that could enhance our existing content, we would love to hear from you.

Was this content helpful to you?

Related Articles